The Fed issued a rate cut this past week, marking the third 25bps cut this year. The Fed continues to balance its dual mandate of maximum employment and stable prices

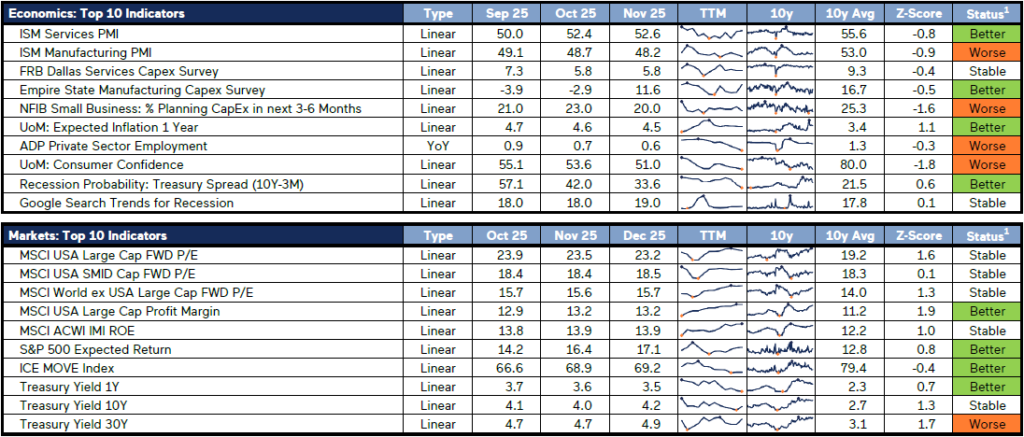

ADP Employment grew at the slowest annual pace since April 2021; and consumers maintain low confidence, especially the bottom third by income

Since end of Q3, the yield curve has steepened, with the 1-year yield down 14 bps and the 30-year up 12 bps, often implying lower recession risk

Services continue to carry the US economy with manufacturing lagging behind, this is the third month in a row that services PMIs have climbed and manufacturing PMIs have declined

Yet recent New York and Dallas Fed surveys show manufacturing firms expect capex growth to accelerate while small businesses are pulling back anticipated capex

US equity returns have slowed down so far in December, stabilizing elevated P/Es; valuations remain historically high but are supported by strong fundamentals

Falling short-term yields should be a good sign for small cap equities with most of the floating rate debt being issued by these firm